Portfolio Update Here

June was not a very good month for my CIS UK Equities fund. Nothing terrible, but still a little annoying as I have been waiting for this fund to transfer into Interactive Investor so that I can manage it properly for around 16 weeks (admittedly the first 8 weeks were lost due to the original transfer form being sent to the wrong address).

I'm getting quite frustrated with this now as I really do need to rebalance a little and take some of the eggs out of that particular basket. Time to make some phone calls ....

Sunday, 29 June 2014

Sunday, 22 June 2014

Cooking with Flair.

As someone who's done all the standard investment reading with due diligence (Tim Hale backed up by Monevator), I have come to the conclusion that I need to explain to myself why I can't just follow the standard recipe for success (low cost passive trackers) but keep on being tempted to add a pince of this and a little of that.

Justifying this to myself is necessary because rationality dictates that I should sell up the large holding I have in my CIS actively managed fund (when it does arrives in II - 16 weeks and counting!!) and redistribute it across a balanced range of passive funds. The statistics are well researched and pretty conclusive. Active funds in general do not beat the market and any particular "top performing" active fund rarely beats the market consistently. Popular fund managers may well outperform for some of the time but there is no guarantee that they will continue to do so and the extra expense of buying active eats away at any extra profit anyway. Case proved.

Instead what I will probably do is to combine shifting a fair amount into the trackers I have already bought (Emerging Markets, Europe and FTSE 250) with putting more money into my Investment Trusts (Heritage - Specialist small IT and comms, Shin Nippon and Aberdeen Small Asian) and also into Fundsmith. In addition I'm likely to be keeping an eye out for likely vehicles for a couple of areas in which I feel under-invested - Europe and the USA (although admittedly I'll probably do this particular one via a tracker). Whatever I do end up doing I know for a fact that I won't be playing it completely by the book.

There is obviously a contradiction here. I understand that If I want to make a loaf of bread I had better follow the recipe. Put in too much salt and it won't rise, forget the yeast and you'll be left with a leaden biscuit. Once mixed, leave the whole thing to rise and do not disturb in the meantime. There is no room for "personalisation". Using passive trackers to make an investment "loaf" follows the same principles. Why do I think that I know better, or worse still, don't seem to care?

I think that most of the tension between what I know I should do and what I actually find myself doing comes from the fact that I believe I'm different from the norm. (Yes, don't we all.) This isn't because I think I'm cleverer, have some gift to pick the right funds or time the market, but I'm different because I have a DB pension waiting in the wings. My staple income for my future, my "daily bread" is already stacked up in the freezer ready for me to take out when I need it. Building a pension fund is not something you would want to mess with and luckily for me I don't get the opportunity to, as my LGPS pension is managed for me and the amount I will receive is guaranteed.

I think that most of the tension between what I know I should do and what I actually find myself doing comes from the fact that I believe I'm different from the norm. (Yes, don't we all.) This isn't because I think I'm cleverer, have some gift to pick the right funds or time the market, but I'm different because I have a DB pension waiting in the wings. My staple income for my future, my "daily bread" is already stacked up in the freezer ready for me to take out when I need it. Building a pension fund is not something you would want to mess with and luckily for me I don't get the opportunity to, as my LGPS pension is managed for me and the amount I will receive is guaranteed.

This doesn't mean that I have given myself carte blanch to be reckless. What I have done is allow myself to be "interested". The whole process will only work for me if I feel like I am having some sort of personal involvement rather than simply following a completely pre-set formula for success which involves throwing all the ingredients into the mix and waiting. Making bread is a particular type of "cooking" - it has an in-built proving time. Things happen slowly, with time as one of the ingredients. This is also true of passive investing.

What I'm doing is more like making a spicy stew to suit my own particular taste buds that will go along with that bread. So I have allowed myself to try a few ingredients of my own along with the staples, being aware of what I am doing and monitoring closely how things are going, tasting all the time and adjusting as required. I'm happy with that.

Justifying this to myself is necessary because rationality dictates that I should sell up the large holding I have in my CIS actively managed fund (when it does arrives in II - 16 weeks and counting!!) and redistribute it across a balanced range of passive funds. The statistics are well researched and pretty conclusive. Active funds in general do not beat the market and any particular "top performing" active fund rarely beats the market consistently. Popular fund managers may well outperform for some of the time but there is no guarantee that they will continue to do so and the extra expense of buying active eats away at any extra profit anyway. Case proved.

Instead what I will probably do is to combine shifting a fair amount into the trackers I have already bought (Emerging Markets, Europe and FTSE 250) with putting more money into my Investment Trusts (Heritage - Specialist small IT and comms, Shin Nippon and Aberdeen Small Asian) and also into Fundsmith. In addition I'm likely to be keeping an eye out for likely vehicles for a couple of areas in which I feel under-invested - Europe and the USA (although admittedly I'll probably do this particular one via a tracker). Whatever I do end up doing I know for a fact that I won't be playing it completely by the book.

There is obviously a contradiction here. I understand that If I want to make a loaf of bread I had better follow the recipe. Put in too much salt and it won't rise, forget the yeast and you'll be left with a leaden biscuit. Once mixed, leave the whole thing to rise and do not disturb in the meantime. There is no room for "personalisation". Using passive trackers to make an investment "loaf" follows the same principles. Why do I think that I know better, or worse still, don't seem to care?

I think that most of the tension between what I know I should do and what I actually find myself doing comes from the fact that I believe I'm different from the norm. (Yes, don't we all.) This isn't because I think I'm cleverer, have some gift to pick the right funds or time the market, but I'm different because I have a DB pension waiting in the wings. My staple income for my future, my "daily bread" is already stacked up in the freezer ready for me to take out when I need it. Building a pension fund is not something you would want to mess with and luckily for me I don't get the opportunity to, as my LGPS pension is managed for me and the amount I will receive is guaranteed.This doesn't mean that I have given myself carte blanch to be reckless. What I have done is allow myself to be "interested". The whole process will only work for me if I feel like I am having some sort of personal involvement rather than simply following a completely pre-set formula for success which involves throwing all the ingredients into the mix and waiting. Making bread is a particular type of "cooking" - it has an in-built proving time. Things happen slowly, with time as one of the ingredients. This is also true of passive investing.

What I'm doing is more like making a spicy stew to suit my own particular taste buds that will go along with that bread. So I have allowed myself to try a few ingredients of my own along with the staples, being aware of what I am doing and monitoring closely how things are going, tasting all the time and adjusting as required. I'm happy with that.

Wednesday, 11 June 2014

Getting the temperature right.

Risk is a vital component in any successful financial plan and attitude to risk is a major factor when considering how to invest. Getting it wrong can mean that the return on the investment is not sufficient, or not at the right level when it needs to be cashed in. Put the pot on too low a heat and it won't cook properly, too high and it is in danger of boiling over.

No-one wants to spend their days wondering why their pot has turned out to be lukewarm and not "cooked through", nor their nights worrying whether it will boil over, or its contents evaporate into the air just when they are needed.

In order to help us with this tricky balancing act questionnaires have been developed that purport to be able to assess our attitude to risk and tell us where we stand on the scale between "batten down the hatches" and "devil may care". Following a link from ermine's post in March, I took the (free) Finametrica test. This is the result:

However I have the feeling that this high score says more about my current stable financial situation, my lack of responsibility for dependants and my "de-mob happy" feeling of being completely debt free rather than saying anything about an underlying personality trait. In other words my risk tolerance isn't an "attitude" at all but rather a reflection of my situation (which does, after all, include a modest, but valuable final salary pension). If I'd taken the test 20, or even 10, years ago I suspect that the result would have been very different.

There is a danger that the results of tests like these tend to stick with us as being true because they are supposed to be about us rather than about how we feel now, in our current situations. As such they could be in danger of being self-fulfilling, especially when coupled with the way investment types are graded into matching categories. In other words, I could take the test at 35, the result comes out as low tolerance to risk and from then on I put my money into investments that "match" my score despite the fact that 10 years later my situation is very different.

Personally I have a tendency to rely on concrete measures in order to inform my mix of investments rather than let myself be led by my "attitude". Maybe it is just that I feel fairly confident that I can count on my ability to research the facts. Perhaps this is a false confidence because it sometimes feels as if the "facts" are pretty hard to find under all the "gossip" out there in the financial press.

However, despite my seemingly reckless base nature (according to Finametrica) my portfolio actually has a low/moderate risk level (according to Trustnet it comes out at 78).

But maybe I should follow my instinct, relax a little, let my true highly risk-tolerant nature shine through and turn up the heat.

No-one wants to spend their days wondering why their pot has turned out to be lukewarm and not "cooked through", nor their nights worrying whether it will boil over, or its contents evaporate into the air just when they are needed.

In order to help us with this tricky balancing act questionnaires have been developed that purport to be able to assess our attitude to risk and tell us where we stand on the scale between "batten down the hatches" and "devil may care". Following a link from ermine's post in March, I took the (free) Finametrica test. This is the result:

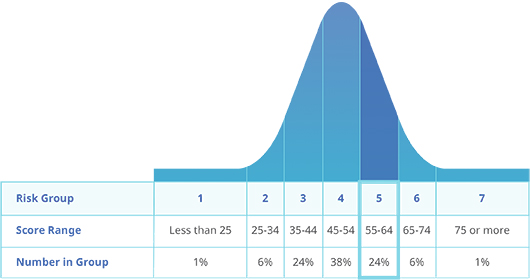

Your Risk Tolerance Score enables you to compare yourself to a representative sample of the adult population. Your score is 64. This is a very high score, higher than 91% of all scores.

When scores are graphed they form a bell-curve as shown below. To make the scores more meaningful, the 0 to 100 scale has been divided into seven Risk Groups. Your score places you in Risk Group 5.

In answer to the last question, you estimated your score would be 58. Most people under-estimate their score by a few points. Yours was a slightly bigger under-estimate. When compared to others you are somewhat more risk tolerant than you thought you were.

However I have the feeling that this high score says more about my current stable financial situation, my lack of responsibility for dependants and my "de-mob happy" feeling of being completely debt free rather than saying anything about an underlying personality trait. In other words my risk tolerance isn't an "attitude" at all but rather a reflection of my situation (which does, after all, include a modest, but valuable final salary pension). If I'd taken the test 20, or even 10, years ago I suspect that the result would have been very different.

There is a danger that the results of tests like these tend to stick with us as being true because they are supposed to be about us rather than about how we feel now, in our current situations. As such they could be in danger of being self-fulfilling, especially when coupled with the way investment types are graded into matching categories. In other words, I could take the test at 35, the result comes out as low tolerance to risk and from then on I put my money into investments that "match" my score despite the fact that 10 years later my situation is very different.

Personally I have a tendency to rely on concrete measures in order to inform my mix of investments rather than let myself be led by my "attitude". Maybe it is just that I feel fairly confident that I can count on my ability to research the facts. Perhaps this is a false confidence because it sometimes feels as if the "facts" are pretty hard to find under all the "gossip" out there in the financial press.

However, despite my seemingly reckless base nature (according to Finametrica) my portfolio actually has a low/moderate risk level (according to Trustnet it comes out at 78).

But maybe I should follow my instinct, relax a little, let my true highly risk-tolerant nature shine through and turn up the heat.

Wednesday, 4 June 2014

Paying My Dues

"Tax Planning" (sic)

A civilised society can be measured to a very large extent by its taxation system and the way it balances the financing of the infrastructure and services that support our daily lives, along against the financial freedom of its citizens.

This balancing act is notoriously difficult to get right as people differ greatly in where they would put the boundaries between the two elements and the weight they would give to each in the equation. I am a socialist and I would rather the see-saw, if it has to tip one way or another, was weighted towards financing the things that benefit us all (education, a free universal health service, the transport infrastructure, welfare) rather than towards allowing individuals to build their own wealth at the expense of those things.

I realise that it is more complicated than this but basically, I believe that we act "better" collectively than we do if allowed (forced) to fend for ourselves. Humans are social creatures, progress through time has so far supported this fact. As we have developed throughout history civilised societies have demonstrated the strength of this basic instinct by creating systems that support the social infrastructure, protect the vulnerable and promote equality and justice. (Although there is an argument that this progress is now being eroded to some extent - one for another day).

In an interesting speech last month Mark Carney, the governor of the Bank of England, warned that "Capitalism is at risk of destroying itself unless bankers realise they have an obligation to create a fairer society". He also said "Prosperity requires not just investment in economic capital, but investment in social capital". Bankers should concentrate less on short term profits (personal greed) and more on the social ethics of their actions. I totally agree.

So how come I find myself working so hard to find ways of reducing my future tax bill, putting money into my SIPP for the tax benefit this brings and getting so annoyed when HMRC get the bill wrong for the tax I owe on my rental property? Surely there's just a hint of hypocrisy there?

Of course all of this is perfectly legal. I'm not a higher rate tax payer (never have and never will be - neither has my husband) so the benefit I get from the tax relief on wrapping my savings in ISAs and pensions isn't that great. I am entitled to tax relief on the mortgage interest on our rental property. At the end of the day I'm only taking advantage of benefits that are available to everyone. But it's a fact that a lot of people just aren't in a position to be able to take advantage of those benefits, or don't know how to. This makes me uneasy.

For most of my life I haven't been able to invest because there just hasn't been the funds, I didn't have money to put into a rental property. I now have more freedom to make more money simply because I have more money. I'm not sure that there is any real freedom at the root of this at all, just luck, good management and fortune, whatever that means (for a lot of people it means "inheritance"). Is that what we should be basing the taxation system on, rather than what we need it to do?

I have no answers and, so long as I can quieten my conscience by giving it the assurance that I am working to the rules, I will continue to minimise my tax burden even though I believe that I should be carrying more of that burden than I actually am.

In the long run, and considering the way things are going under this current government, I may well turn out to be the poorer for not being bound by tighter taxation rules. Rules that force me to carry more of that burden. I suspect that I will end poorer because I will be living in the kind of society I cannot abide.

A civilised society can be measured to a very large extent by its taxation system and the way it balances the financing of the infrastructure and services that support our daily lives, along against the financial freedom of its citizens.

This balancing act is notoriously difficult to get right as people differ greatly in where they would put the boundaries between the two elements and the weight they would give to each in the equation. I am a socialist and I would rather the see-saw, if it has to tip one way or another, was weighted towards financing the things that benefit us all (education, a free universal health service, the transport infrastructure, welfare) rather than towards allowing individuals to build their own wealth at the expense of those things.

I realise that it is more complicated than this but basically, I believe that we act "better" collectively than we do if allowed (forced) to fend for ourselves. Humans are social creatures, progress through time has so far supported this fact. As we have developed throughout history civilised societies have demonstrated the strength of this basic instinct by creating systems that support the social infrastructure, protect the vulnerable and promote equality and justice. (Although there is an argument that this progress is now being eroded to some extent - one for another day).

In an interesting speech last month Mark Carney, the governor of the Bank of England, warned that "Capitalism is at risk of destroying itself unless bankers realise they have an obligation to create a fairer society". He also said "Prosperity requires not just investment in economic capital, but investment in social capital". Bankers should concentrate less on short term profits (personal greed) and more on the social ethics of their actions. I totally agree.

So how come I find myself working so hard to find ways of reducing my future tax bill, putting money into my SIPP for the tax benefit this brings and getting so annoyed when HMRC get the bill wrong for the tax I owe on my rental property? Surely there's just a hint of hypocrisy there?

Of course all of this is perfectly legal. I'm not a higher rate tax payer (never have and never will be - neither has my husband) so the benefit I get from the tax relief on wrapping my savings in ISAs and pensions isn't that great. I am entitled to tax relief on the mortgage interest on our rental property. At the end of the day I'm only taking advantage of benefits that are available to everyone. But it's a fact that a lot of people just aren't in a position to be able to take advantage of those benefits, or don't know how to. This makes me uneasy.

For most of my life I haven't been able to invest because there just hasn't been the funds, I didn't have money to put into a rental property. I now have more freedom to make more money simply because I have more money. I'm not sure that there is any real freedom at the root of this at all, just luck, good management and fortune, whatever that means (for a lot of people it means "inheritance"). Is that what we should be basing the taxation system on, rather than what we need it to do?

I have no answers and, so long as I can quieten my conscience by giving it the assurance that I am working to the rules, I will continue to minimise my tax burden even though I believe that I should be carrying more of that burden than I actually am.

In the long run, and considering the way things are going under this current government, I may well turn out to be the poorer for not being bound by tighter taxation rules. Rules that force me to carry more of that burden. I suspect that I will end poorer because I will be living in the kind of society I cannot abide.

Sunday, 1 June 2014

Subscribe to:

Comments (Atom)